Who is the best VC in the world?

A list of lists of the best VCs

Everyone loves rankings (especially rankings of VCs). And everyone loves a listicle. Why not combine them? What could be better than a listicle which ranks the best lists of rankings?

Our holiday present to our readers is a compilation of lists to identify the best VCs.

Which lists did we miss? Feel free to add in the comments.

Top 5 list of the best lists of the best VCs

1. Midas List

The Forbes Midas List is the gold standard of VC lists. VCs fight tooth and nail to be on this list. It represents strong firm & personal branding, with a knock-on effect on deal flow and fundraising.

Here is Forbes describing their methodology:

A data-driven ranking, the Midas List is produced annually from a combination of public data sources and the submissions of hundreds of investment partners across dozens of firms. To qualify, investors are ranked by portfolio companies that have gone public or been acquired for at least $200 million in the past five years, or that have at least doubled their private valuation to $400 million or more over the same period.

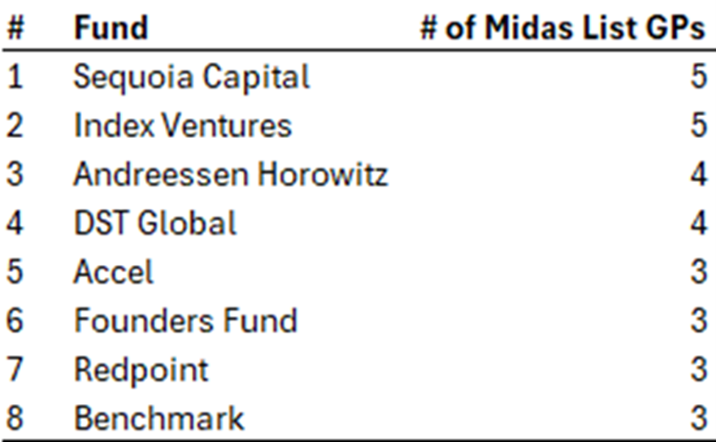

The Midas List is at the individual GP level but it obviously generates reflected glory for the firm itself too. Here is the list of all firms with three or more GPs on the 2024 Midas List (Figure 1).

Figure 1. Firms with 3+ GPs on the 2024 Midas List

If there was a criticism of the Midas List, it would be that the Midas List is a little stale. For example, the #2 on the 2024 list is Ribbit’s Micky Malka for his investment in Coinbase when he first invested in the Series A in … checks notes… 2013. Totally understood that VC investments take time to mature, but maybe a more up-to-date methodology could be helpful?

For the 2024 Midas list, the mean date of seed round for companies selected by Forbes was 2015 (Figure 2).

Figure 2. Key dates for 2024 Midas List companies

Here is the full list of companies selected by Forbes in the Midas List (Figure 3):

Figure 3. All companies in the 2024 Midas List

Midas also has a brink list, seed list and Europe list.

2. Signalrank.ai

We publish our ranking of VCs at every stage from pre-seed onwards here. This is updated automatically daily.

Over a rolling five-year window at each round, we consider a variety of factors, including the investor’s average MOIC for the last 5 years, investment efficiency (unicorn percentage among investor’s investments), and the number of unicorns in which they have invested.

This is at the firm level. We also have a GP-level list internally; we do not publish this GP list as the publicly available data at the GP level is not as rich as at the firm level (in part because some firms choose not to ascribe investments to individual partners).

Folks seemed to like our list of all investors in 10+ unicorns from seed investments (Figure 4) which we published in July.

Figure 4. SignalRank’s list of investors in 10+ unicorns from seed

3. Peer review: top VCs as selected by other VCs

Eric Newcomer came across this interesting list of the top VCs as selected by other VCs (Figure 5). It is not systematic or scientific but it is instructive of how VCs perceive other VCs.

Figure 5. Venture Manager Survey

4. Founders’ choice of VCs

In 2022, Eric Newcomer also published this list of the “Founders’ Choice” of firms, asking founders to vote anonymously on which investors they’d be most inclined to take money from again. This is the updated version of the list.

Landscape created a similar founder’s choice list here with a more European focus.

5. Investors who backed $5bn+ outcomes

DST’s Cole Rotman recently published this matrix of who invested in the Series A of companies which went on to deliver $5bn+ outcomes (Figure 6). The full Google sheet is here.

Figure 6. VCs who backed Series A of $5bn+ outcome companies by year of Series A

Other lists

DealRoom: this list breaks down VCs by looking at unicorns at seed, Series A, Series B+ and future unicorns. They also look at rankings by geography, as well as the number of unicorns backed over time by age of firm.

HEC & Dow Jones: HEC created their third annual list of the best performing VCs. The methodology is somewhat opaque.

Kauffman Fellows: this aims to look at fund performance. It tends to focus more on emerging managers.

PitchBook: Pitchbook separately looks at most active and best performance across multiple alternative asset classes.

Preqin: similar to Pitchbook, Preqin has league tables here across multiple asset classes

Crunchbase: Crunchbase reviews the most active VCs per quarter here

Sovereign Wealth Fund Institute: this ranking purely looks at the top VCs by capital raised.

Venture Capital Journal: this looks at who has raised the most amount of money in each year.

Icarus List: Founders Fund’s John Coogan suggested (somewhat tongue in cheek) the creation of an Icarus List of VCs who lost the most amount of money in any year.

What have we learned?

The big brands are strongly represented on these lists (especially Sequoia, Benchmark, Index, A16Z, Founders Fund, USV, and Accel).

Is anyone surprised? No. Did we see any unexpected names? Probably not. Is this the worst sort of navel-gazing? Almost certainly.

But there might also be an important point hiding among this growing multitude of lists, as well as potential clues about the future shape of the venture ecosystem.

The big brands are overrepresented within these lists to the potential detriment of micro VCs. These lists can and do have an impact on brand building which in turn can impact deal flow and fundraising.

According to PitchBook here, this year has seen the top 30 VC funds raise 75% of all venture capital in the US (Figure 7).

Figure 7. Top 30 firms raised $49bn in 2024

There is a clear flight to perceived quality (read: brands) among allocators in 2024. This data set from Equidam’s Dan Gray (Figure 8) demonstrates that in 2024 the top 10 VCs by fund size raised more than 50% of all VC dollars in US for the first time.

Figure 8. Share of US Venture Capital funds raised by year

Micro VCs and emerging managers are fighting for their position in the ecosystem. The best managers will continue to raise capital, but it looks like the much anticipated Great Reset in VC is well underway.

Precursor’s Charles Hudson considered three potential future states of the ecosystem, as multi-stage funds park their tanks on the seed managers’ lawn (Figure 9). This is an important discussion to be had.

Figure 9. Precursor considers the future of seed investing

It feels unlikely that we return to the pre-ZIRP state of affairs with clear swim lanes between multi-stage funds and seed only funds.

In 2025, seed managers need to make the case for how they are differentiated and for their distinct value in the ecosystem. This is a particularly challenging question in the midst of the platform shift to AI where the investment norms for VCs are yet to be fully established (where we argued here that it is still very early in AI’s development).

It is going to be fascinating to see this play out in 2025 and beyond.

In the meantime, Happy Holidays!