Investing in AI: 10 VC strategies to watch

VCs are in the arena trying stuff. Some will work, some won't. But always learning.

This is not investment advice and is for informational purposes only. Investors should conduct their own research.

The days of paint-by-numbers VC investing are over. Software investing over the last ten years has been straightforward (although not necessarily easy), with a stable tech ecosystem powered by the twin growth engines of cloud & mobile, all while enjoying low interest rates & a relatively benign geopolitical backdrop. This approach distilled to the triple triple double double formula to building a $1bn company. Simples.

The advent of the capex intensive AI era, coupled with the poor performance of unprofitable SaaS companies which went public in 2021 (within a much changed subsequent macro environment), has disrupted the cozy investing model described above.

A new platform technology requires a recalibrated investment approach (and likely revised business models). Especially given the enormous capex required to establish leading edge foundational models. SoftBank’s Masayoshi Son has talked about how a $9 trillion (trillion with a t) capex investment into AI is “too small”. How does a mid sized VC play in a $1bn foundational model round?

We are at the dawn of this next technology wave. Things are moving quickly. But we have argued here how it is still early in the current cycle, especially for VCs, where making early investments can be tantamount to being wrong. Sequoia echoed this recently by discussing how there’s a blank space for AI apps.

This flux in VC’s legendary pattern recognition skills creates opportunity. With investing norms yet to be fully established for investing into AI, we are witnessing a flourishing of different approaches to how best to play AI, from grant giving to investing in not-for profit structures, to chip leasing strategies and beyond. In other words, investors are, like Chamath Palihapitiya, “in the arena trying stuff. Some will work, some won’t. But always learning.” 😎

We will canter through ten different ways we see investors seeking to capitalize on the newest new thing. We will see that there are many ways to play the game, with different strokes for different folks. We will then bring this line of thinking closer to home, by considering how a new platform technology could impact SignalRank’s own style of investing.

10 AI investment strategies

This will be ordered by stage, from inception through to public markets. These are examples of strategies, designed to illustrate that different investors are taking different paths when approaching AI investments. This is by no means comprehensive and by no means represents making any kind of recommendation.

For each investor, we highlight AI companies picked by these investors which could also qualify for SignalRank’s Series B product (post Series A companies with signal which we call “Candidates”), as well as later stage companies which would have qualified for SignalRank’s product when they raised their respective Series B (“Qualifiers”). In addition, we flag companies already in the SignalRank Index (where we have backed our seed partner to finance their pro rata in a qualifying Series B).

1. Indexing the earliest stages: NFDG

Nat Friedman (former CEO of GitHub) and Daniel Gross (former YC partner; now co-founder of Safe Superintelligence) have been active in supporting AI research since 2017, when they first started grants for AI projects. This grant program continues with grants of up to $50,000 in compute or cash. Their investment strategy has expanded beyond grants to becoming an active accelerator ($250k in uncapped SAFE) and early stage investor ($1m to $100m investments). They were ranked #6 on Eric Newcomer’s list of VCs ranked by other VCs.

NFDG AI portfolio companies rated by SignalRank:

Candidates (13): Accord, Anysphere, Atomic AI, Character.ai, Consensus, Dagger, Distyl AI, Deepnote, Doppler, Glide Apps, Granola, Reka AI, Safe Superintelligence

Qualifiers (14): Airplane, AssemblyAI, Deel, Digits, ElevenLabs, Klarity, Perplexity, Pika, Polywork, Retool, Scale AI, Socket, Strapi, Vercel

SignalRank Index (1): Pika

2. Thought leadership & access to European talent: Air Street Capital

Nathan Benaich, based in London, is the founder & GP of Air Street Capital, which is investing in AI-first technology and life science companies. He has been writing the excellent State of AI annual report since 2018. Air Street has been investing from “day 1” in AI companies since 2019.

Air Street Capital AI portfolio companies rated by SignalRank:

Candidates (2): anagenex, Contextual AI

Qualifiers (3): poolside, intenseye, Synthesia

3. Outsourced VC fund for AI founders: Factorial Capital

Matthew Hartman, formerly partner at Betaworks, launched Factorial Capital in 2023 as a $10m fund backed by Clément Delangue, cofounder and CEO of AI platform Hugging Face. The fund partners with angel operators and write checks of around $100,000 on average into AI companies. By partnering with AI founders, Hartman has strong access to next generation founders. Other examples of AI operator backed funds include Depth Capital Ventures, Pebblebed and Theory Forge.

Factorial Capital AI portfolio companies rated by SignalRank:

Candidates (6): Adaptive ML, Factory, Flower Labs, Modal Labs, Nomic AI, Patronus AI

Qualifiers (2): Perplexity, Pika

SignalRank Index (1): Pika

4. Using AI to invest in AI: Basis Set Ventures

Xuezhao Lan set up Basis Set Ventures with the goal of leveraging technology (with their Pascal system reviewing 10k+ companies) to invest in seed stage AI-enabled software companies. Basis Set raised their third fund of $185m last year. Basis Set also made the list of managers that other VCs would want to invest in (see similar comment for NFDG above).

Basis Set AI portfolio companies rated by SignalRank:

Candidates (9): Dynamo AI, Facet, Norm AI, Playbook, Rutter, Sakana AI, Series, Trendsi, Whimsical

Qualifiers (3): Drata, Rasa, Scale AI

5. Back the right founders at (almost) any cost: Khosla Ventures

Khosla Ventures backed OpenAI in 2018 with a $50m check which was “an easy decision to make”, even for an initial check which was 2x Khosla’s largest initial investment in 40 years. This was also despite the funky non-profit structure (and capped upside for investors) at the time: “Those are details. There are multiple non-profits in Europe with for-profit arms.” Back the right founders, and the rest will sort itself out.

Khosla AI portfolio companies rated by SignalRank:

Candidates (12): Arpeggio Bio, Ava, Daedalus, DevRev, Ello, Moonwalk Biosciences, Nabla Bio, Nomagic, Sakana AI, Sarvam AI, Symbolica AI, WindBorne Systems

Qualifiers (20): Abacus.AI, Atomwise, Berkshire Grey, Bidgely, Cape Analytics, Caption Health, Clear Labs, CloudTrucks, Curai Health, Lumiata, Novi Connect, Paravision, Pymetrics, Sword Health, SymphoneAI Sensa, Tempo, TrueAccord, Upstart, Vahan, Zebra Medical Vision

SignalRank Index (1): Vahan

6. The Everything Store: asset accumulation (plus grants & chip leasing): A16Z

Marc Andreessen has gone from believing that “software will eat the world” to proclaiming that “AI will save the world”. With a cool $6bn in fresh powder (including 15% earmarked for AI infrastructure), A16Z has been and will continue to be an active AI investor. While A16Z has invested in OpenAI, A16Z has been a strong advocate & investor (as well as grant donor) for open source AI projects. The latest initiative is to support startups with access to GPUs via its Oxygen program.

A16Z AI portfolio companies rated by SignalRank:

Candidates (16): Anysphere, Braintrust Data, Character.ai, Distributional, Doppel, Fal.ai, Hippocratic.ai, Ideogram, Kaedim, Rewind AI, Rezo Therapeutics, Safe Superintelligence, Series Entertainment, Spade, Valar Labs, Viggle AI

Index companies (40): Alation, Alluxio, Anyscale, BigHat Biosciences, Captions, Coactive AI, Cresta, Databricks, dbt Labs, Decagon, Deepcell, DeepMap, Doxel, Drishti, ElevenLabs, Genesis Therapeutic, Infinitys Systems, Insitro, Instart, KoBold Metals, Labelbox, Mistral AI, Motherduck, Overtime, People.ai, Pindrop, Rasa, Replicate, Ribbon Health, Rigetti Computing, Saronic, Shield AI, Sift, Sisu, Skydio, Socket, Symbio Robotics, Tennr, Waymo

SignalRank Index (1): Saronic

7. Buying a seat at the table via secondaries: Thrive Capital

Thrive Capital has established itself as one of the most successful new VC brands over the last 15 years and currently manages north of $15bn.

Thrive’s bold secondary investment strategy into OpenAI (in rounds in both February and September this year) has echoes of DST Global’s famous $200m investment for a c.2% stake in Facebook at a $10bn valuation in 2009. DST’s investment was considered to be wildly profligate at the time. Likewise, Thrive’s valuation on OpenAI of $157bn has got folks talking. Could this be the first $1tn AI company?

By establishing itself as a major AI player with its $1bn+ investment into OpenAI, Thrive should see some ancillary benefits with additional dealflow at the earlier stages.

Thrive AI portfolio companies rated by SignalRank:

Candidates (13): Anysphere, Cloud Health Systems, Command AI, Cursos, Essential AI, Fabric, HeyGen, Lightspark, MEDIVIS, Nourish, Samara, Savvy Wealth, Scope Security

Qualifiers (3): Gong, Guru, Scale AI

8. Strategically important corporate VC: NVIDIA

NVIDIA and its VC arm, N Ventures, have been active in making venture investments since at least 2016. This has ramped up significantly since NVIDIA became the darling of the AI boom, with 84 AI VC investments to date. NVIDIA can also provide superior access to their chips for their portfolio companies, leading to some accusations of roundtripping of revenue.

NVIDIA AI portfolio companies rated by SignalRank:

Candidates (5): Essential AI, Inceptive, Sakana AI, Superluminal Medicines, Together AI

Qualifiers (13): Adept AI, Aya Labs, Cohere, Cohesity, Fireworks AI, Heavy.ai, Iambic Therapeutics, Luma AI, Mistral AI, Perplexity, Poolside, Scale AI, Skydio

9. Unlimited balance sheet – Microsoft

Microsoft’s partnership with OpenAI has provided the AI leader with access to Microsoft’s almost unlimited balance sheet.

It is an understatement to state that this has been a strategically important investment for Microsoft, as it battles the other Magnificent 7 players in the quest for AGI. Packy McCormick has covered how the Magnificent 7 are all playing Pascal’s Wager with AI. He quotes Google’s Larry Page as saying “I am willing to go bankrupt rather than lose this race [to create a Digital God]."

Microsoft AI portfolio companies rated by SignalRank:

Candidates (6): Agolo, DatologyAI, Ema, Foundry, HiddenLayer, Wallaroo

Qualifiers (11): Databricks, d-Matrix, Everstring, Innovaccer, Inworld AI, Markforged, SCUBA Analytics, Synack, Tact.ai, Typeface, Unstructured Technologies

10. Sovereign wealth – Abu Dhabi

The capex required to build next gen foundational models means that deep pocketed sovereign wealth funds are likely to critical roles in the development of AI. Middle Eastern SWFs have been particularly adroit in positioning themselves for this technology cycle.

Saudi Arabia has a dedicated AI fund and is talking about a $40bn partnership with A16Z to invest into AI. Yet it is the Abu Dhabi which is currently the sovereign at the leading edge for AI investments. Abu Dhabi created MGX, a technology investment partnership with Mubadala and G42 as the foundational partners. MGX has already announced an AI infrastructure partnership with BlackRock & Microsoft, aiming to raise up to $100bn for data centers and other AI infrastructure. All while Mubadala continues to invest in AI companies from its US & European funds.

Mubadala AI portfolio companies rated by SignalRank:

Qualifiers (5): Insitro, Innovaccer, People.ai, Unlearn,ai, Waymo

BONUS – public & quasi-public strategies

The secondary markets for late stage private companies (dubbed quasi-public companies by Altimeter’s Brad Gerstner) can provide investors with direct (well, via SPVs) access to specific leading names. It is not so challenging to find vehicles which provide access to OpenAI, xAI, CoreWeave, Waymo, Figure AI, Replit and others.

Likewise, investors who believe that the current phase of AI favors incumbents could do worse than to invest in the Magnificent 7 (Amazon, Apple, Tesla, Google, NVIDIA, Meta & Microsoft), who have invested a cumulative amount of $75bn into AI/ML since 2020 (according to 7GC estimates here).

Finally, large credit shops (including Blackstone, Pimco, Carlyle and BlackRock) are engaging in AI by lending capital to neocloud companies who provide cloud computing to tech groups building AI products. These necloud groups, such as CoreWeave, Crusoe and Lambda Labs, have acquired tens of thousands of NVIDIA chips which is used as collateral for huge loans. $11bn has been lent with this strategy to date.

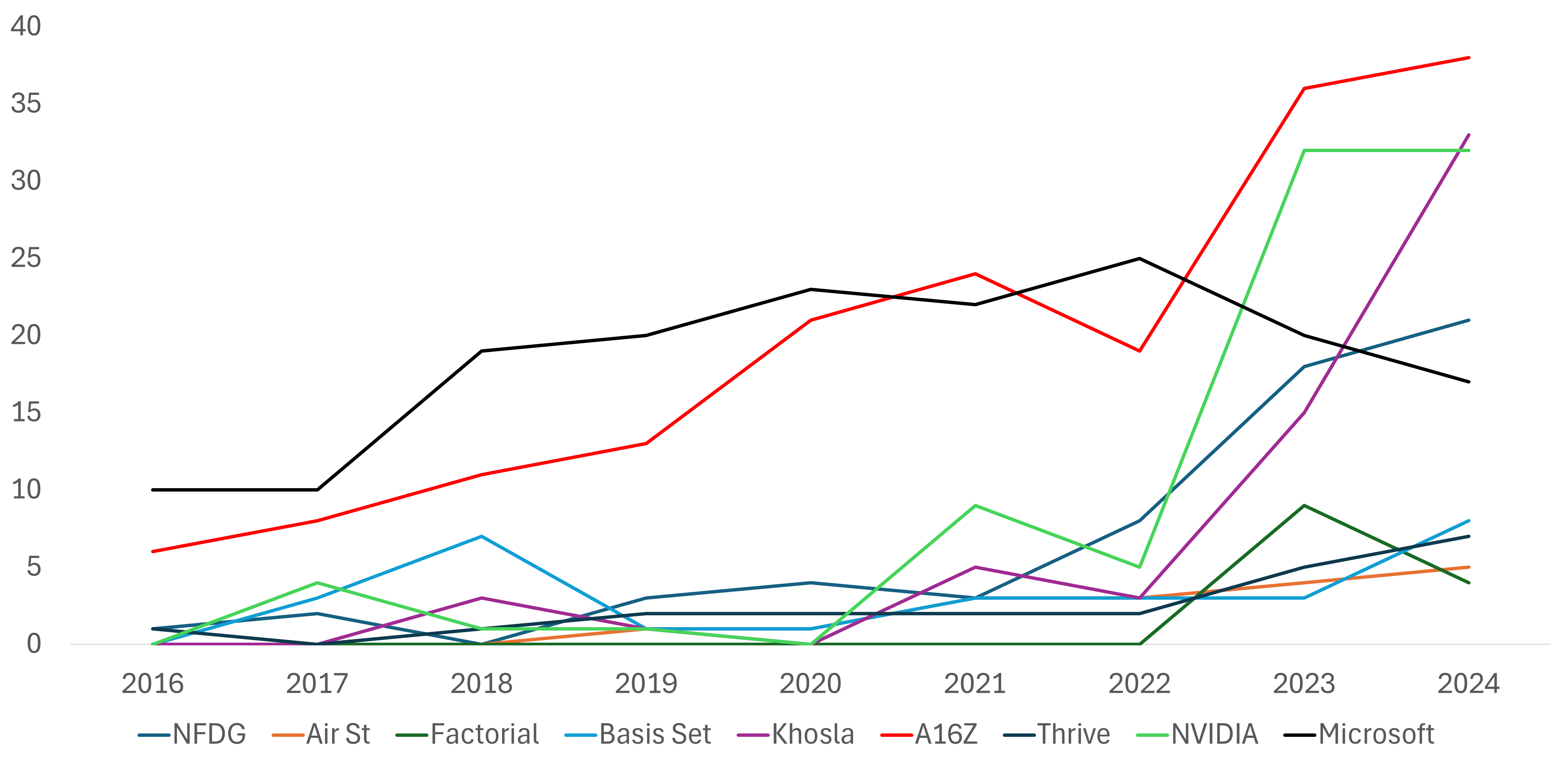

AI investments per annum per strategy

Here is a chart to show how investments by style are ramping up (Figure 1). Note the recent growth in number of investments by NVIDIA and by Khosla.

Figure 1. # of AI investments per annum per investor (2016-24)

Source: Crunchbase (with AI investments per Crunchbase grouping)

What does this mean for SignalRank?

SignalRank exclusively invests in companies selected by our proprietary algorithms, where the company had previously raised capital from high quality investors and is raising a top 5% Series B per our algorithms.

The biggest risk to our strategy is that the style of early stage investing changes. The previous mobile & cloud cycles benefitted from relatively capital efficient models (with low capex requirements thanks to AWS et al) and standardized unit economics metrics. This allowed for staged, almost programmatic, investing style with well-defined round dynamics. Founders & investors alike understood the alphabet soup, from seed to Series A, Series B, Series C, etc.

Software investing over the last ten years has been a Goldilocks strategy for VCs, requiring neither too much nor too little capital. The new paradigm of AI could upset this dynamic.

At one end of the spectrum, building foundational models is capex intensive. Too capex intensive for most VCs. $100bn is mooted for a next gen model. At the other end of the spectrum, AI will write much of the software itself, making human engineering teams much more efficient (Google recently announced that 25% of their new software is written by AI). There is much talk of someone creating the first one person $1bn+ valued company. Software engineer job listings are already in decline. With minimal capital, it could be possible to create the next herd of (profitable) unicorns. In either scenario, it is unclear what role (if any) a VC would play.

We are yet to see either scenario play out. Instead, the New New Moats framework outlined by Greylock’s Jerry Chen seems more realistic. The new AI startups may be able to build product with minimal (zero?) engineers, which will therefore require less capital and fewer rounds. But companies still need to master go-to-market. “AI doesn’t change how startups market, sell or partner. AI reminds us that despite the technology underpinning each generation of technology, the fundamentals of business remain the same. The new moats are the old moats.”

In other words, companies will still need to raise capital to take their product to market. Hiring marketers, sales teams, talent partners, legal teams & finance departments all requires equity capital. Indeed, from the ten investment strategies introduced above, you can see that a large number of companies have already been flagged at Series A as having signal (“Candidates”) and that many AI companies have raised Series Bs which would have qualified for our product (“Qualifiers”). In 2024, we expect there to be around 100 qualifying Series Bs globally, most of which will be AI companies.

We still need to guard against complacency. But for now it appears that SignalRank’s strategy of investing in the “third round” of a company to deliver risk-adjusted consistent returns across the Index can be sustained in the age of AI.