What flavor of capital do you want?

VC brands: authenticity supersedes professional & polished patter

This is not a post about politics. But the US election illuminated how capital has become personified, reflecting the values and outlook of individuals (not firms). So the election feels like a good place to start to understand this shift from firm-level brands to individual platforms.

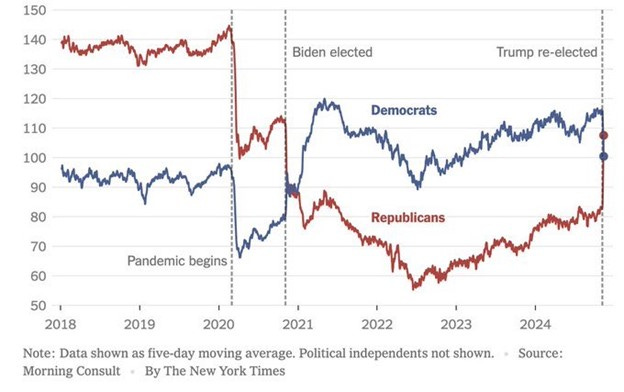

Social media has weaponized information to such an extent that society is now struggling to agree on basic facts. This chart (Figure 1) on consumer sentiment by party identification would be funny if it wasn’t so concerning. Consumer sentiment has become so polarized that views on the economy function as a kind of political Rorschach test.

Figure 1. Consumer sentiment by party identification, 2018-24

The politicization of information has now infected capital too. The recent election illuminated glaringly different interpretations of the world within the VC community.

It is particularly intriguing that VCs have engaged in more forthright political discourse in this election cycle on both sides, as one would imagine that VCs are looking for the best founders regardless of their political affiliation. Y Combinator’s Paul Graham tweeted about how “VCs have the strongest incentive not to discriminate of any group in the world.” He went on to argue that “if multiple companies founded by Martians with eyes on stalks started growing really fast, VCs would be falling over one another to invest in more companies founded by Martians with eyes on stalks. You know they would.”

Yet here we are. On team Trump, we had Doug Leone, David Sacks, Keith Rabois and Peter Thiel. On team Harris, we had Reid Hoffman, Vinod Khosla, Ron Conway and Aileen Lee. Pick your fighter.

The most fascinating dynamics are where firms were divided at the personal level. This could be interpreted as a hedge of some sorts to not aggravate entrepreneurs of one tribe or another. You could also argue that this represents a firm level maturity where individuals can disagree agreeably under the same umbrella. A16Z had Trump-supporting Marc Andreessen pitted against Ben Horowitz who switched at the last minute to Harris. The partner meetings at Lux Capital must be tense given the opposite positions taken by Josh Wolfe and Bilal Zuberi (who has subsequently left to found his own firm) on Gaza. Tim Draper sidestepped an election position entirely by endorsing both candidates. Nice.

Yet a slide into ever further polarization among the VC community is not a fait accompli. Nat Friedman astutely observed “pessimists sound smart, optimists make money.” Innovators, regardless of political affiliation, tend to be preternatural optimists.

Aaron Levie, CEO of Box and vocal Democrat, recognized this after the election by tweeting: “Wild ride. Congrats to @realDonaldTrump on becoming President again. What’s great about America is that we’re on a rocket ship right now and can keep accelerating with the right policies and execution.” Greylock’s Reid Hoffmann echoed this in the FT recently: “some of my peers in Silicon Valley who supported Trump in this election did so in the belief that his administration will strike a pronounced innovation-friendly stance. If they’re right, and I hope they are, then we should see more competition, faster improvement and fewer efforts to dictate goals and outcomes in complex, fast-evolving high-tech industries.”

Beyond politics

There is actually something much more interesting happening here beyond political jockeying. The center of gravity for VC brands has shifted from the firm level to the individual GP.

VC corporate brands have become bland to the point of absurdity. This video from Redpoint is excellent on how VC websites are meant to make you feel. Who’s isn’t founder friendly these days? Who isn’t excited about AI?

The staleness of the corporate brand is in stark contrast to the vibrancy of personal platforms. This reflects the transition from the traditional one-to-many media environment (TV & radio) to a more chaotic many-to-many media environment today (social media). Many individual GPs command larger audiences than their corporate firms (Marc Andreessen’s 1.7m X followers are double A16Z’s 800k X followers). Are you even a VC if you don’t have a podcast these days?

In our time, authenticity (warts and all) supersedes polished & “professional” patter. This is true in VC and politics alike.

There is, however, a paradox that direct access enables the public to touch and feel individuals more closely than in previous environments, while simultaneously also reducing the aperture for nuance. A single tweet or like can be (often wrongly) extrapolated to a whole platform of personal values.

Correlation Ventures has shown that the value of a venture capital firm is little more than the value of the individual GPs. By decoupling an individual’s brand from the corporate brand, social media is a catalyst to the rise of solo GP funds. See the success of Harry Stebbings in raising capital for 20VC. It is reminiscent of the truism espoused by Justin Kan among others that “first time founders are obsessed with product. Second time founders are obsessed with distribution.” Build an audience & capital base that align with your goals and personal values.

The growing supermarket of solo GPs enables you to go for pure, unadulterated, and concentrated flavors of capital that suit your particular taste and signal your own personal values.

Therefore, what?

The atomization of opinion in the broader public is reflected in the VC community. A diversity of viewpoints is healthy and should be encouraged.

Yet indices aim to reduce bias and risk to approximate the mean of their target asset class. Vanguard’s John Bogle talked about how “index funds eliminate the risks of individual stocks, market sectors and manager selection, leaving only stock market risk.” Should we add the personal values of managers to this mix?

Our index is blind to the personal values of the underlying GPs. It purely looks at objective investor performance over time. But this performance obviously includes embedded bias of the make up of the set of Patagonia-wearing GP constituents.

Social media has surfaced the personal values of individual investors whose brands are now more prominent than those of their corporate employer. Perhaps we need to be mindful that our index should aim to reflect a heterogeneous set of personal values by underlying GPs.

In the end, VC is a very long game, where short-term hot takes by VC are noise. Character, judgement and investment track record are important; a position on one issue or another is usually not. I am reminded of the FT’s Janan Ganesh on avoiding reading contemporary books as the best books survive the “filtering effect of time”. So should the best VCs.