State of the Series B ecosystem

2024 report

We are excited to share here our second annual report on the state of the Series B ecosystem.

The SignalRank Index reflects the top 5% of Series Bs in terms of MOIC potential, with our Series B investments completed in support of our seed partners (who are existing investors in these companies and wish to exercise their pro rata rights). As such, understanding the Series B ecosystem is critical to our business model.

In this post, we will consider how broader trends impacted the Series B ecosystem, as well as tease out some preliminary conclusions from the report.

We hope you enjoy the report.

The broader context

In 2024, the Series B market was impacted by a number of core broader themes in the technology sector, including:

AI domination The foundational models have continued to improve, while the hyperscalers invest ever more capital into AI infrastructure, research and product. According to CB Insights, 2024 has seen 72 companies become unicorns, and 32 of these (44%) are AI startups. These AI players are reaching unicorn status far faster (median of 2 years) than non-AI companies (median of 9 years).

Liquidity remained elusive While the stock market boomed and interest rates fell, this is yet to translate into IPOs. The rise of private tender offers and continuity funds reflect the persistence of the IPO drought. There were just nine venture-backed IPOs above $1bn valuations in 2024. The success of ServiceTitan’s listing reveals substantial public investor demand for high growth software. Encouraging for 2025.

Concentrated VC fundraising In 2024, 30 firms raised 75% of all capital raised by VC funds in the US, demonstrating how the tech pullback is concentrating influence among a small number of venture brands.

Silicon Valley’s government takeover People used to complain about the revolving doors between government and Wall Street. The importance of Elon Musk’s role in Trump’s election has led to similar noises being made about the influence of Silicon Valley (especially the ex PayPal crew, including Elon Musk, Peter Thiel, and David Sacks). While yet to take office, the impact of Silicon Valley’s central role in government is already starting to be felt (most visibly in crypto markets).

Preliminary conclusions from the report

AI has arrived in Series B land

There is a clear bifurcation in Series B land between AI companies and non-AI companies. AI companies are raising more rounds, larger rounds, at higher valuations and from higher quality investors than their non-AI peers.

Companies founded since the launch of ChatGPT in late 2022 are now starting to raise Series Bs in earnest. xAI alone raised $6bn for its Series B in 2024, just $1bn shy of the aggregate amount raised in all Series Bs globally in 2012 ($7bn).

The overall number of Series Bs fell by 6% compared to 2023 to 1,144 (in-line with 2014 levels of activity). But the average round size is the highest of any vintage, as AI today is a capital intensive technology.

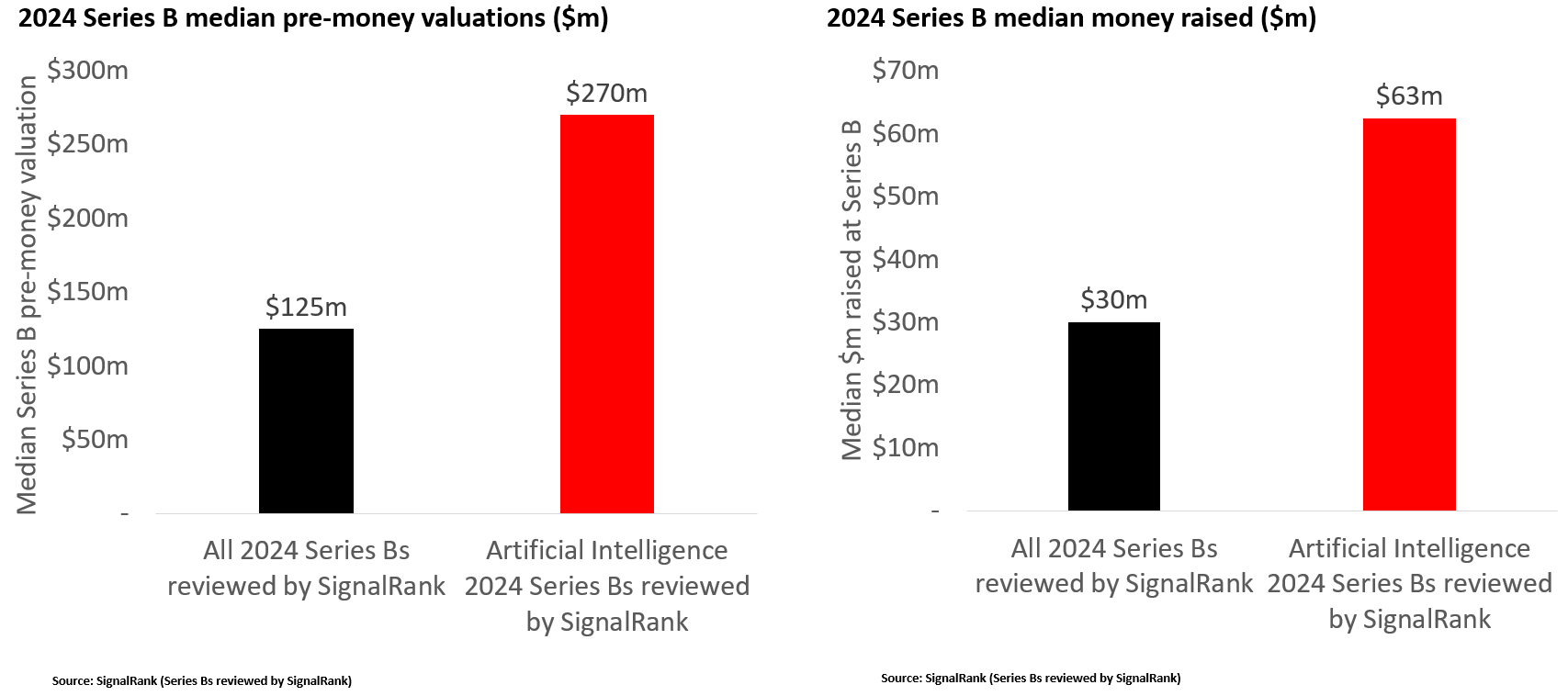

The split between AI and non-AI companies is seen most visibly in terms of valuations and round sizes (Figure 1).

Figure 1. Median pre-money valuations & capital raised in 2024

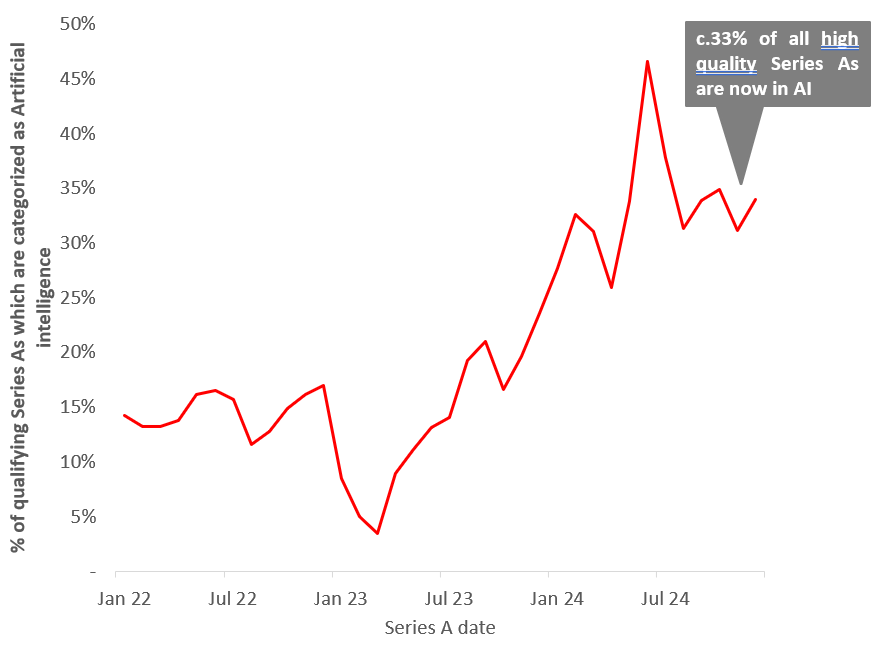

SignalRank tracks the highest quality Series As which become ‘candidates’ for the SignalRank Index. The pipeline of good Series As is robust, and has swung in earnest towards AI too. The consistency of candidate generation suggests a decent pipeline of Series Bs over the next three vintages (Figure 2).

Figure 2. Percentage of qualifying Series As per month in AI

Source: Crunchbase

Best investors are actively investing

A16Z remains the most active Series B investor globally, with 29 Series Bs completed in the last 12 months (Figure 3). A16Z is followed by Y Combinator, Lightspeed, Bessemer and General Catalyst. SignalRank was the eighth most active investor in 2024 with 14 completed investments.

Figure 3. Most active Series B investors in 2024 (by # of investments)

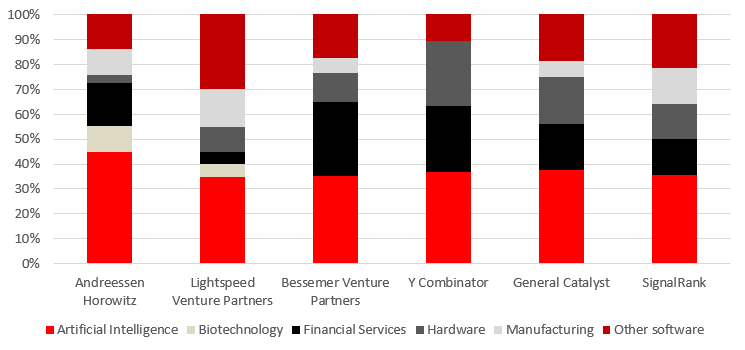

The focus of these active investors is primarily on US AI (Figure 4).

Figure 4. 2024 Series Bs by sector (% of 2024 Series B investments)

Source: Crunchbase

By analysing how investors are co-investing at Series B in 2024, we see the network centrality of high frequency Series B investors (Figure 5). This filters for investors who made 10+ Series B investments in 2024, with edges demonstrating 2+ co-investments.

This chart demonstrates how the most highly networked investors are reflecting high quality Series B beta. SignalRank is at the center of this group by design, demonstrating that our systematic approach is delivering consistent access to companies backed by high quality active investors.

Figure 5. 2024 Series B network centrality

Source: SignalRank

Growth investing & liquidity remain subdued

Series C conversion (& unicorn creation) remains subdued (Figure 6). <10% of Series Bs are raising Series Cs within two years (compared to c.30% in pre-2022 years). We anticipate that this trend continues until liquidity returns.

Figure 6. Percentage of Series Bs which raise a Series C

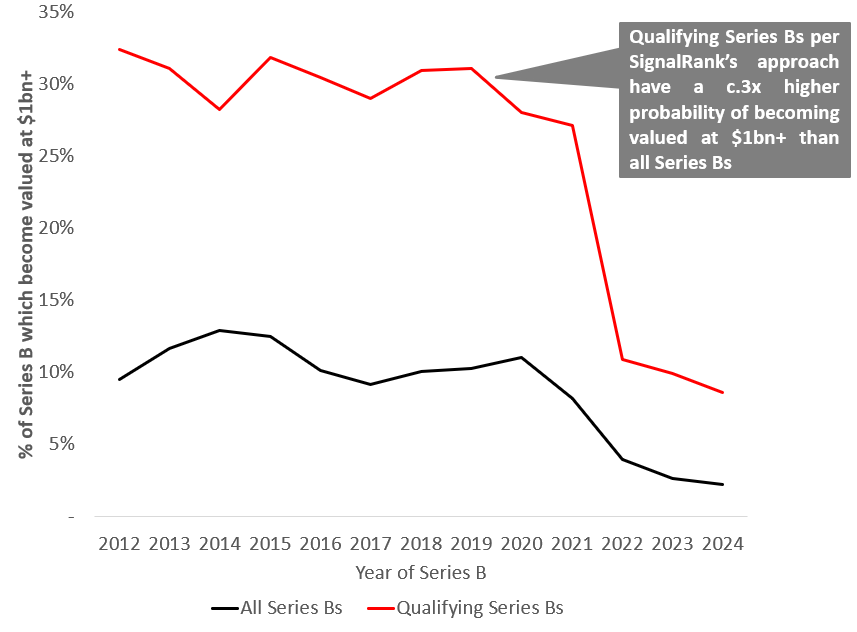

While Series Cs in general are at low levels, SignalRank’s ongoing backtest shows that qualifying Series Bs (per our methodology) are consistently more successful in raising subsequent rounds and in resulting on $1bn+ valuations (Figure 7).

Figure 7. Percentage of Series Bs which become valued at $1bn+ (2012-24)

Source: SignalRank; Crunchbase

Concluding thoughts

The technology sector is all-in on the development of artificial intelligence. We are in the midst of the largest capital allocation to any single technology in human history. This is being reflected (in a small way) at the Series B stage, where the highest potential companies founded in the last two years are raising sizeable rounds in quick succession.

The election of Trump and his coterie of Silicon Valley bros has led to a return of the animal spirits in the public and crypto markets. We anticipate this has a positive spillover effect on the private tech market in 2025, from VC fundraising to Series B activity and to liquidity events.

This is not to negate a Trump administration’s general unpredictability, together with the potential risks seen in the geopolitical sphere (especially Ukraine, the Middle East & Taiwan) or the impact of any US tariffs on the global economy.

Yet, overall, the combination of a thriving technology cycle (in AI) and a positive public market outlook makes us optimistic for the Series B ecosystem in 2025.